What is the annual payslip and why is it relevant to my tax return?

The annual payroll certificate is more than just a simple annual payroll statement. It in fact is an essential part of your annual tax filing. The payroll certificate includes all relevant documents per employer that pertain to the respective year. If you have different employers during a year you will receive an annualy payroll certificate per employer.

Please note: If you are employed in a Mini-job, please note that mini-Jobs typical do not get an annual payroll certificate because social security contributions and wage tax are not paid.

When do you receive your annual payslip?

In general employees receive the annual payroll certificate anytime between December and February of the following year. If there are delays, consult your employer.

If you resign from a company during the year, (in many cases) your former employer will send you the annual payslip earlier than usual. If you have received unemployment benefit (Arbeitslosengeld) for any duration during the tax year, you’ll also receive it from the employment office as a payroll tax statement (Lohnsteuerabrechnung). This usually arrives by the end of February.

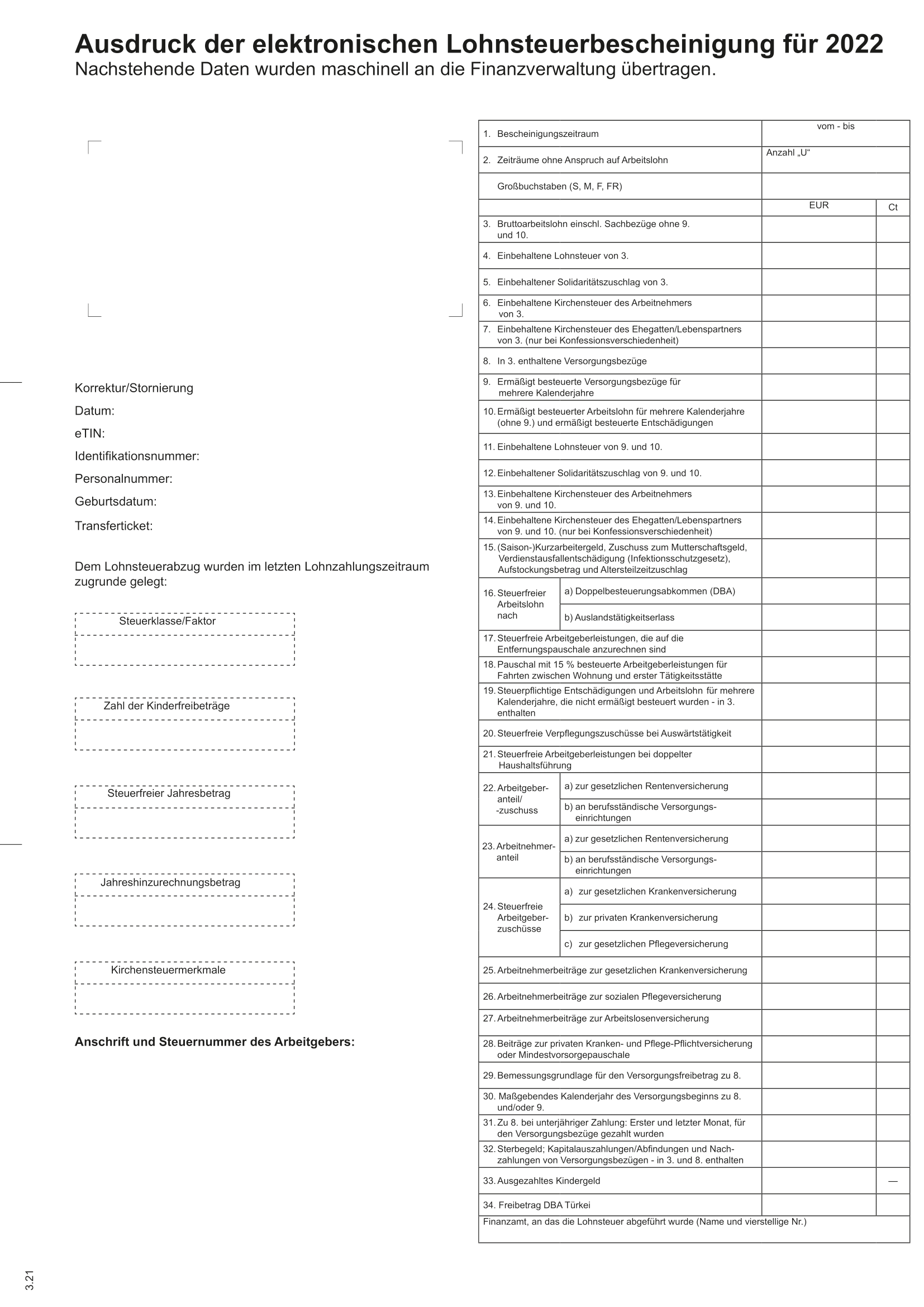

Annual Payslip in Detail:

On the printout of the annual payroll certificate you will find a lot of information about your income and your personal tax characteristics in 2 columns:

You will find the following information on the left column:

The employee’s earnings and deductions for the past year are listed on the right-hand side of the certificate. The positions for the information are numbered.

1. Certification Period: The period to which this wage tax statement relates, i.e. during which the employee worked for the company, is specified here.

2. Periods without entitlement to wages: If the employee has not been entitled to wages for more than 5 consecutive working days, the number of these days is indicated after the capital letter „U“.

3. Capital letters (S, M, F, FR)

4. Gross wages including benefits in kind: The gross wage is listed here.

5. Withholding Tax: The wage tax, like the solidarity surcharge (5) and the church tax (6), is calculated on the basis of the gross wage.

6. Withheld solidarity surcharge

7. Withholding Church Tax

8. Retained church tax of the spouse/life partner (in the case of different denominations)

9. Pension benefits included in gross wages (3): Pension payments that are part of gross wages are, for example, income that is comparable to a pension and is paid by the employer or a company pension and benefit institution.

10. Reduced taxed pension payments for several calendar years: This includes, for example, additional payments for a period of more than twelve months. They are taxed preferentially using the fifths rule.

11. Reduced taxed wages for several calendar years and reduced taxed compensation: Under certain conditions, wages can be taxed at a reduced rate. It must then be reported separately from the rest of the salary. This comes into question, for example, in the case of benefits from the employer on the occasion of an employee anniversary or in the case of a severance payment.

12. Withholding payroll tax from 9 and 10

13. Retained solidarity surcharge of 9 and 10

14. Employee’s church tax withholding from 9 and 10

15. Church tax withheld by spouse/domestic partner of 9 and 10

16. (Seasonal) short-time work allowance, maternity benefit allowance, etc. The sum of the following tax-free benefits is listed here: short-time work allowance, allowance for maternity allowance, allowance in the event of an employment ban for the time before or after childbirth and for the day of childbirth, compensation for loss of earnings under the Infection Protection Act as well as top-up contributions and surcharges for partial retirement.

17. Tax-free wages: Payments for a foreign activity that are exempt from wage tax either according to the double tax agreement (16a) or the foreign activity decree (16b) are listed here.

18. Tax-free employer benefits to be credited against the commuting allowance: If the employer pays or subsidizes the journey between home and first place of work, this is noted here.

19. Flat rate taxed employer benefits for travel between home and first place of work: The employer can also tax the amount that the employee claims as a flat-rate distance allowance in their tax return at a flat rate of 15%.

20. Taxable compensation and wages for several calendar years that were not taxed at a reduced rate (included in 3): Compensation and wages for several calendar years that are not taxed as in 10 are entered here.

21. Tax-free meal allowances for external activities: In the case of external work, the employer can grant the employee a meal allowance of up to 24 euros. The sum of these grants is listed here.

22. Tax-free dual household benefits: The sum of the contributions that the employer replaces tax-free in the case of double household management is given here. This includes travel expenses, additional meal expenses, expenses for the second home and moving costs.

23. Employer contribution/subsidy: The employer’s contribution or subsidy to the statutory pension insurance (a) and, if applicable, to the professional pension scheme is given here.

24. Employee Share: In addition to the employer’s contribution, there is also the employee’s contribution to statutory pension insurance (a) and, if applicable, to the professional pension scheme.

25. Tax-free employer grants: The employee receives a tax-free subsidy from the employer for statutory health insurance (a), private health insurance (b) or statutory long-term care insurance.

26. Employee contributions to statutory health insurance: The contributions paid by the employer for statutory health insurance are listed here.

27. Employee contributions to social long-term care insurance: The contribution to social long-term care insurance paid by the employer is shown here

28. Employee contributions to unemployment insurance

29. Contributions to private compulsory health and long-term care insurance or a minimum flat-rate provision: In the case of private health insurance, contributions are listed here that the employer takes into account when deducting wage tax.

30. Basis of assessment for the pension allowance for 8

31. Relevant calendar year of the start of the supply at 8 and/or 9

32. For 8 in the case of payments during the year: First and last month for which pension benefits are paid

33. Death benefits, lump-sum payments/severance payments and back-payments of pensions – included in 3 and 8: The amount of the pension payment in special cases, such as death benefits, is listed here.

34. Paid child benefit